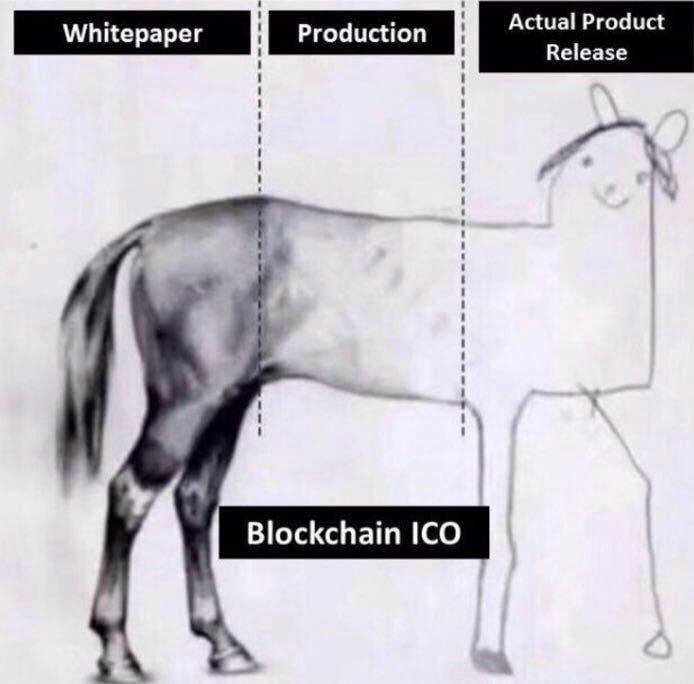

Why we didn’t ICO

By Aleks S

Because we love our users, and don’t want to rip them off.

We also give a $%*& about our business — and some stupid token created for the sake of raising non-dilutive capital will just get in the way of running the business, create pointless friction, increase the barrier to entry, confuse the end user, undermine our actual product and…that’s just got no integrity.

It’s a cash grab. And that’s not what we’re here for.

A project like Amber does not need a “Blockchain” or “Token” to function.

In fact, that someone would do an ICO just to raise capital shows where their true motivation lies.

Jimmy Song’s article sums it up perfectly in the “Venture Capital and Bootstrapping” section:

Perhaps the most successful thing that “blockchains” are good at is raising money from the public via ICOs. Not only are the terms of these ICOs exploitative of the buyers, but they’re heavily manipulated through premines, pay-for-exchange listings and other morally questionable activities.

Obviously, the companies selling the tokens like getting money, but the conditions under which they’re sold give the investors almost no protection whatsoever. This not only hurts the investors who have no guarantee of any good or service ever coming to them, but also hurts the companies that raise money this way.

I strongly recommend you read it:

So why didn’t we do an ICO?

Well, there is a number of over-arching reasons:

But, before we even talk about why we didn’t, let’s discuss why a “business” running an ICO with a utility token is a ridiculous idea in the first place.

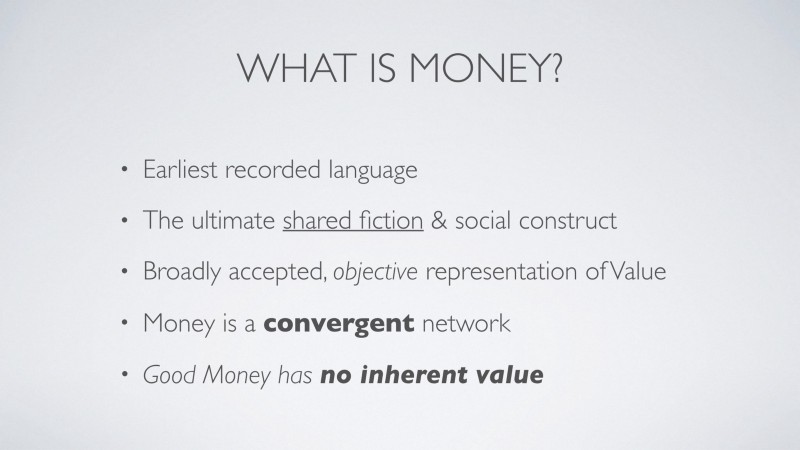

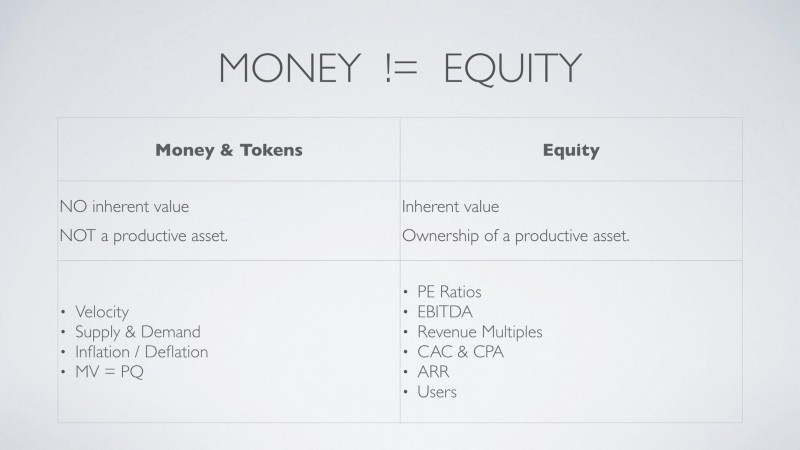

1. Money != Equity

Tokens behave like money, and money does NOT behave like equity.

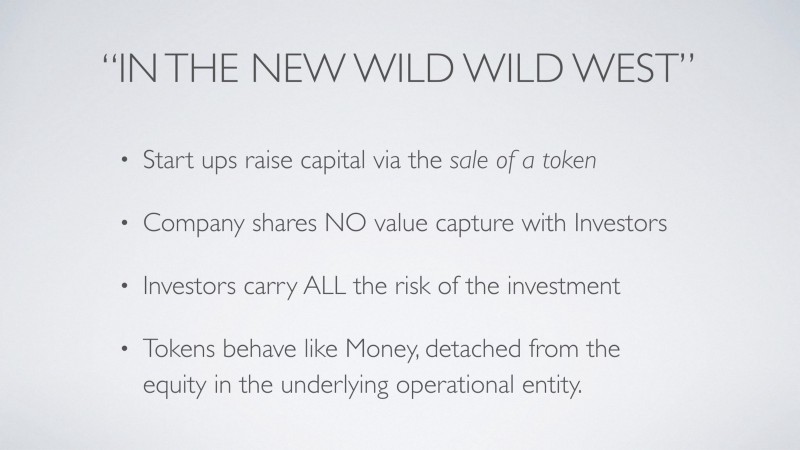

When companies (or foundations) are raising capital via an ICO, the investor is not buying any of the company they are buying a token that will ‘one day’ pay for work on the network, and thus functions like a currency upon that network.

The creators of these ICO’s then go about the process of developing an “economic model” for that token, whilst spinning the narrative that the “retail investors” of the world can now participate in early stage investments via a token sale.

There is a significant problem here.

These foundations/ groups/companies raising an ICO are NOT selling equity, rights or ownership of ANY form in the underlying operational entity. And it’s especially bad when the idea is a “business”.

These capital raises are non-dilutive.

This means that, as an investor, you are not buying equity, nor are you participating in the same economic framework that equity operates within.

You, as an investor, are buying “money” — and money has no inherent value. Not only that, but with the proliferation of exchanges and a globally interconnected world, a network like money tends to converge to unity.

It’s outside of the scope of this article for me to discuss money in further depth, so as a one-stop reference, please read this article:

So if people are actually investing in a form of ‘money’ (which has no inherent value) on a network that will hopefully one day be built, or worse; for a business that is not yet functional, where that unit of account is NOT related back to the underlying operational entity what’s to stop the consensus on that “money” converging to zero?

Well… nothing really except a continuation of the “greater fool theory”.

The reality of the fact is that people buying tokens in ICOs are giving these creators money for air. They’re hoping the creators of this token (a) stick around in the first place, and (b) actually have the ability to build a robust enough economic model for the price of the token to appreciate in value (which nobody in history has ever been able to do), not to mention justify why the token should even have value in the first place.

The realisation that this is hard is only just starting to occur. And as it continues, a lot more money will be lost until investors wake up, stop buying air and stop conflating the different economic models of equity and money.

The following sums up the core differences:

I would strongly also recommend everyone reads this by Brendan Bernstein:

So….

Now that we have that out of the way, let’s dig further into why we didn’t do an ICO (or DTS / TGE and whatever else they’re trying to call it these days).

Integrity

Oh man

Is integrity lacking in this industry!

If anything makes me angry in life, or in business; it’s hypocrisy.

Bitcoin and digital currencies rose up in the aftermath of the Global Financial Crisis, as a response to the fraudulent activity participated in by the banks and financial institutions of the world, who got greedy.

Furthermore, it was a public “stand” made against the rampant money printing, credit creation and inflationary bias of the governments and central banks.

Here we are, barely 10yrs later, under the guise of “decentralization” and “libertarianism”, creating digital money out of thin air, backed by absolutely nothing other than a stupid “whitepaper” and a telegram group, selling it to people who think they’re somehow participating in the next global revolution.

Are you kidding me?

This stuff drives me nuts.

I used to think Tone Vays was a bit too negative, saying everything was a scam — but over time, I’ve come to agree with him.

And one might say: “Hey. Not everyone is a scammer”. And in general, I would agree. But even the non-scammers, who think they’re doing the right thing, are unknowingly selling people shit they don’t even understand themselves!

And I’m sorry, but for me; that’s a sign of a lack of integrity.

So back to our thought process:

1. Raising the right kind of Capital

I’m a big believer of doing things right, from the beginning.

If you have a valid idea, and a viable concept for a business — it’s not hard to raise money.

Whilst I agree that this might not be true in Benghazi or a lot of the non-western world; it doesn’t change the fact that people are investing in over-valued air with no recourse / rights back to the operational entity.

If you’re in a jurisdiction where you have the mechanisms to raise capital in a way that investors are buying something real; then that’s what you should do. And if every investor is “not interested”, then maybe you need to change your approach, adapt, improve, or just realise that your idea (or ability to execute) may just not be that great.

A company raising capital, especially a business that is looking to capture value in a market, should be sharing that value capture with the investors.

The following 2 slides from my presentation sum it up:

Next…

2. Product or Economy?

Startup’s are HARD.

As a business, we asked ourselves; are we here to build a product / business or try to manage an economy?

Why, in the name of Satoshi, should we waste our time worrying about how to manipulate the economic levers of our network so that our tokens don’t pump, dump or get de-listed from an exchange?

As an investor, you should be asking the above. Where should your founders focus go?

- Building an MVP, getting to market, refining the product-market fit, generating revenue and scaling up… or;

- Trying to build a stable ‘economy’; something economists have not been able to do since the day economics was invented, but something the crypto world believes a couple of young coders in a garage who know nothing about economics will somehow ‘figure out’.

So… We decided to build an amazing product. We’ll leave the economics to the people who know what they’re doing.

3. Exchange Listings

Speaking of exchange listings; why in the name of Nakamoto should we give SOOO much power to an exchange, and at such an early stage?

And why in the hell would we spend millions of the dollars given to us by “investors” on an exchange listing?

Is that where the money should go?

These groups are trying to be Apple or Microsoft before they’ve even built a product! Have any of us truly matured enough as companies to worry about “listing”, already?

No Way.

It’s just more insanity.

4. Regulation

Again. Startups are hard!

Time is finite, resources are limited. Where is that time, energy, money and focus going?

ICOs, despite what the loopholes some lawyers have tried to navigate through, are securities. There is no two-ways about it. And trying to sell an unregistered security is a BAD idea (made worse by selling air).

So again — we’re here to build a product — not to try and find legal loopholes on how to raise non-dilutive capital or go to jail in the process.

5. End User / Customer

In a similar vein to the above, we’re here to build a great product with a simple mission:

“To make digital currencies easy, for everyday people.”

Why would we introduce a token in the middle of it all? That would just confuse the crap out of the customers, and draw in speculators who don’t give a shit about the product, won’t even use the product, and in the process screw up any mechanism of “utility” we may have tried to impart on the token for the end user.

It’s just stupid.

6. Mis-alignment of Values

As a business, as a team, as an organization; it’s your values that align you — with the internal stakeholders (ie; team, investors, founders) and with external stakeholders (i.e. users, partners, promoters).

Trying to align all of these is difficult enough as it is. An ICO does not make any of that easier.

Our mission, as described above, is simple:

And in order to execute it, we need to play the long game. We need to maintain a long-term vision and do the right thing when it counts, for all stakeholders.

Which ties in with my next point:

7. Fundamental value VS speculative hype

With all the above in mind, what are we really trying to build and which option aligns most with our values?

If you, like me, subscribe to the idea that the real growth in this industry/technology is yet to come, then it follows that long-term thinking is required.

Long-term value capture requires both time and trust.

A highly volatile, easily manipulated token is in direct contrast to all of the above!

8. Strong Foundations

Large corporate companies are often beaten by small, nimble startups that can do more with less.

In saying that, whilst large corporates with lots of money are slow and cumbersome, they’ve had time to build systems and procedures that bring some form of efficiency into the operations.

Startups, that raise SOOOOOOO much money that they don’t know what to do with it, end up building the wrong kind of company. The excess capital available teaches them to just throw money at problems.

It’s the worst of both worlds. It’s a startup with no systems and procedures (low efficiency) and lots of money and therefore resources to manage (low efficiency), so you end up with low efficiency squared.

I couldn’t think of a more ridiculous way to build a business.

Jimmy Song sums it up perfectly again:

Lack of money is often a forcing function for finding a path to profitability. What many of these companies have instead are ungodly sums of money without much motivation to actually solve problems as there’s no accountability. Many become investment funds that try to outsource actual innovation by funding other companies to develop on their platform. These, too, are often ICOs and thus have no obligation to actually build. What you end up with are lots of rent-seekers with not much reason to create.

There’s a reason government programs to spur “business activity” very rarely result in good businesses. Money that’s granted without much accountability tends not to be spent very well.

9. Zero… ZERO need for a token

Last but not least, as a business, we have NO need for a token. Zero. Zip. Zilch. And neither does anyone doing something similar to what we’re doing!

If they are — it’s a blatant cash grab, and just proves where their intent lies (or if they have a good intent, they’re just stupid and therefore poor stewards of people’s money and trust).

I was asked so many times last year:

“Why don’t you do a token sale / ICO? It would be so easy; you’d raise millions overnight!”

To which my response generally was:

“Well… we don’t really need a token. I would just be making it up for the sake of raising money, which is not right.”

And to my dismay, most would say: “That’s ok just do it anyway”.

I must admit there were times where I seriously thought about it. I even wrote half a “white paper”, with a token model similar to Binance and Huobi. But there were a couple things that stopped me:

- I read 20 whitepapers over a weekend, and by the end of it I honestly felt like I had dropped 20 IQ points. The crap they spun, and the the absolute blindness of the claims and non-understanding of economics just made me cringe.

- A utility token like this, is not great for business. It basically brings the revenue forward and creates a kind of debt obligation the company is supposed to fulfil long-term. For the users (or buyers of the token) they then have to hope the company is still around to redeem these, whilst the speculators want whoever is running it to manipulate the token price in a way that drives its value upwards.

It was those 2 realizations that drove me to really have a long hard think about the long-term ethical, economic, moral and functional aspects of doing an ICO. And I’m glad we didn’t.

This section could blow out for another 2000 words, but I’m going to save that for a future article. For now, you can check this out:

and:

Conclusion

I could go on and on and on — because there are more reasons than what I’ve stated, but I think this is comprehensive enough.

I hope anyone reading understands why we didn’t do an ICO, but more importantly I hope that the path we’ve taken inspires other entrepreneurs with cool ideas to go down the path of raising capital ethically, aligning their values with the investors, end users and all the stakeholders involved.

On the flip side, if regulators are reading this — I hope they can give more thought to how they allow companies and projects to raise capital for their ideas in ways that are legitimate (i.e. sale of equity) in a form that is more global, natively digital and available to the “every day person”.

Whilst it’s clear that I don’t like ICOs, there is good and bad in everything.

The promise of retail investors being able to participate in investments that are traditionally reserved for the “elite” or “sophisticated” of the world is a good thing, and if the next model of token allows for this to occur for investments that are ethical and economically sound, then I’m all for it.

We hope to be involved in doing things the right way, having learnt from what went wrong in this last mania.

I will also note that I understand some protocol-level concepts could argue that they have a requirement for a token. I don’t directly dispute this, and I recognise that in some cases, it might be needed. Although I do question whether or not those things make for good investments (I definitely don’t think they do). But that’s for another article.

Further Resources:

There was a number of great resources that helped me form my thoughts on this topic. Some were linked to above, and some more are below:

Michael Flaxman nails it in his seminal piece breaking down why ICOs are such a bad investment model.

The trade-offs are not worth it, and it’s a false economy, creating liqudity in the begining when there realistically should be none.

He describes it as a cash grab — and it’s a way to literally rip off the very customers they say they want to serve.

Elad Gil is always on point:

Robert Leshner from Compound is another great example.

One of my favourite quotes, and something I completely agree with:

“We shunned an ICO. We said, ‘let’s raise venture capital.’ I’m a very skeptical person and I think most ICOs are illegal,” Leshner notes.

If you enjoyed this post, please show it some love, give it a clap (or a few) and pass it around to anyone you think should have a read.

Hope you got some value and feedback is always welcome!